Contents

Established fund managers are about to witness the largest accumulation and movement of wealth the world has ever seen. PwC projects global AuM to reach $200 trillion by 2030, with private markets generating more than half of all asset management revenues. More investors are entering the space, and the volume of structures required to serve them continues to grow.

Private markets are no longer constrained by capital or demand—they’re constrained by execution. Moving into new markets and asset types adds cost and complexity at a pace older operating models were never designed to handle. As activity accelerates, the real test becomes how much operational load a firm’s infrastructure can absorb without slowing. The industry’s cost-to-income ratio remains stuck at around 68%, after improving from 63% in 2019–2020 to 59% in 2021 before rising again in the following years, a sign of the drag created by systems that haven’t kept pace with rising activity. Operational strain is becoming as central a challenge as commercial growth.

Our Established Fund Manager Report highlights the same pattern. The data points to an industry where the strength of a firm’s infrastructure is becoming a clearer marker of leadership. The question now is how firms choose to respond.

Complexity is rising faster than operating models can absorb

You can see the pace of the market picking up, particularly as private markets expand and capital formation accelerates, a theme reflected in BlackRock’s 2025 Chairman’s Letter.

Fink points to a growing mismatch between global investment demand and the capital available from traditional sources, pushing more financing into the markets themselves. He also notes that roughly $25 trillion sits idle in deposits and money-market funds. These are short-term funds invested in cash-like debt, capital that will need new structures to move through.

But the infrastructure supporting most managers hasn’t kept pace. Much of the industry is still built on foundations designed for a slower market, where activity follows a predictable sequence and information is accessed through tightly controlled, siloed systems. As expectations move toward broader transparency and faster information flow across organisations, those older structures begin to show their limits.

At the same time, technology enables teams to act earlier in the fund’s cycle. Real-time data and automated workflows support continuous execution. Meanwhile, LP portals and emerging AI tools allow firms to handle higher volumes of investor activity and fund operations without manual handoffs or reconciliation.

Diversification isn’t a strategy—it’s survival

Capital no longer enters private markets through one channel. It moves across strategies, wrappers and jurisdictions at the same time, and that movement brings real operational weight.

You can see this in the way demand is evolving. Alternatives AUM is growing at roughly 7% a year and is on track to represent over half of industry revenues by 2030. But the more telling signal is how advisors are behaving. Research by AssetMark shows that 91% of advisors now view access to private markets as critical for differentiation, 68% of those not yet offering alternatives plan to add them within a year, and more than half would switch firms to gain that access. More than 70% of investors who haven’t yet used alternatives say they would allocate resources to private markets if their advisor recommended it.

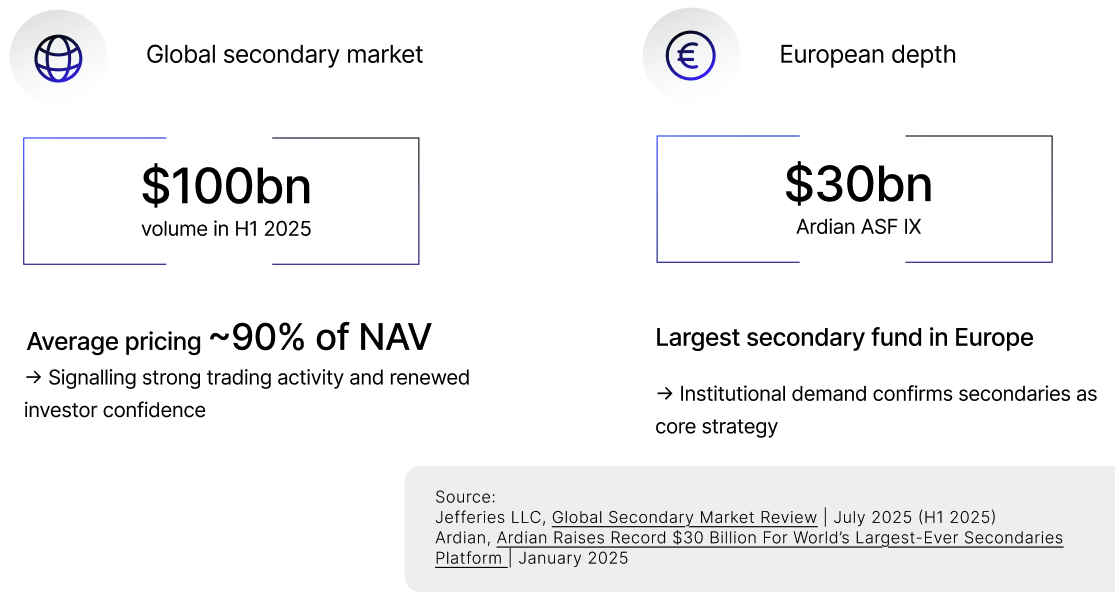

Liquidity cycles show the same pattern in market behaviour. The secondary market reached $100bn in the first half of 2025, and pricing near 90% of NAV shows how quickly portfolios now change hands. Each turnover asks for clear visibility on exposure and capacity at the moment it happens. Industry reports link this rising velocity to structural demand as fee pressure in mutual funds and ETFs pushes firms toward private markets.

The execution gap is widening (and investors feel it)

Execution slips when semi-liquid structures push work across teams and systems that were never meant to work in sync. MUFG’s 2025 analysis of semi-liquid activity shows how these products create more touchpoints and more moments where teams need to act, and investors feel it when those workflows don’t connect.

The real friction shows up in the handoffs. Semi-liquid activity triggers updates, cash movements and approvals that hit different parts of the organisation at different times. When the data doesn’t line up on its own, teams stop to reconcile what should already be clear. Investors see this immediately.

As wealth transfers from Baby Boomers to a new generation of investors—an estimated $80–100 trillion, the largest wealth transfer in history—expectations are shifting. This new cohort is driven by immediacy and purpose, and they expect to see returns and capital transfers within their own lifetimes. That makes timely, consistent visibility into portfolio activity a baseline expectation, not a differentiator.

Why systems built for stability struggle in a world that rewards flexibility

Larry Fink’s 2025 Chairman’s Letter shows a market accelerating on all fronts. Capital is moving beyond the old 60/40 model, where portfolios are split between public equities and bonds, and into private assets, large-scale infrastructure and modern retirement products. Yet trillions still sit in cash, waiting for vehicles that can deploy it with more speed and confidence.

That acceleration translates into real operational requirements:

- Portfolios must rebalance across public and private exposures as the “50/30/20” market structure takes hold, with capital spread across equities, bonds, and private assets.

- Retirement products need to absorb private credit and infrastructure while still respecting liquidity, valuation and fiduciary constraints.

- Capital has to reach new projects at the pace demand sets, not the pace end-of-quarter processes allow.

- Tokenisation and better private-markets data can open faster channels, but only if firms can reconcile positions, entitlements and risk across old and new systems in near real time.

Fink frames this as democratisation: more investors, more access, more ways to participate in private markets. Operationally, it becomes a test of adaptability. Systems built for static allocations and clean separation between asset classes were not designed for products that move across those boundaries by default.

This is why semi-liquid structures reveal strain so quickly. They are trying to operate in the world the letter describes, while running on infrastructure that still assumes stability is the norm.

What leading established managers are doing differently

Based on the growth we’ve seen with Motive Partners, Laton Ventures and Collective Ventures, the firms pulling ahead are the ones rethinking how their execution actually works. They’ve rebuilt how their operating models run day to day, and that’s what keeps things steady as activity rises. In practice, that means:

- Keeping all data in one system, so answers aren’t rebuilt from scratch.

- Processing activity when it happens, shrinking the gap between information and action.

- Recording context inside the model, reducing informal decision-making and preserving continuity.

- Removing sequential handoffs, so workflows move cleanly across teams without delay.

- Using a single operating spine across vehicles, preventing activity from fragmenting across structures.

- Running onboarding as a live workflow, allowing data and approvals to progress continuously through multiple closes.

These changes signal a broader evolution in how firms compete. Execution is now a source of strategic strength, and those who recognise it early are already laying the groundwork for what’s ahead.

The next decade belongs to firms that can evolve their operating identity

What defines strong operations is changing in private markets. An emerging investor base pay close attention to how clearly firms operate, how quickly they act and how reliably their systems hold together as activity increases.

The established managers pulling ahead are the ones evolving their operating identity: they prioritise adaptability over static efficiency, bring intelligence into the centre of their workflows and rely on infrastructure that works as a single system rather than a collection of tools.

This is where the advantage of a stronger operating model becomes visible. As demands rise, the way a firm runs its operation says more about its discipline and ambition than anything else. Operational excellence increasingly forms part of a fund’s identity and reputation, shaping how confidently it can raise capital and how credible it appears to investors. Ultimately, it serves as a critical USP for attracting new investment and raising successfully with LPs. The managers who understand this early are already putting the next decade’s foundations in place.

Download the Established Fund Manager Report for a closer look at the signals shaping this transition.

The best already build on bunch

.webp)

.webp)