Launching a venture capital or private equity fund in the UK involves navigating complex regulatory and operational requirements. Fund sponsors must establish a compliant structure, secure the necessary regulatory approvals, and ensure ongoing adherence to Financial Conduct Authority (FCA) rules. Post-Brexit changes and evolving regulations add further challenges, making it crucial to take a structured approach.

For emerging managers, one option is to work with a host Alternative Investment Fund Manager (AIFM). These regulated entities can act as the manager of your fund, assuming responsibility for portfolio and risk management. By partnering with a host AIFM, fund sponsors can accelerate their market entry while simultaneously working toward obtaining their own FCA licence, creating a more efficient path to launch.

Why Work with a Host AIFM?

A host AIFM is an FCA-authorised entity that takes responsibility for portfolio and risk management under the UK Alternative Investment Fund Managers Regulations (“AIFMD”). By partnering with a host AIFM, fund sponsors can operate under its regulatory umbrella, avoiding the time-consuming and expensive process of securing direct FCA authorisation (and also giving themselves a period of operating with an experienced partner before breaking out on their own).

Engaging a host AIFM allows fund managers to significantly reduce regulatory complexities, speed up their fund launch timeline, and concentrate on their investment strategy—all while maintaining full compliance with UK regulatory frameworks.

Key Areas of Oversight for a Host AIFM

- Capital Raising & Investor Onboarding

- Fundraising Communications: Support with FCA-compliant fundraising communications

- Investor Classification: Professional Client vs. Retail categorisation processes

- Due Diligence: KYC/KYB and AML assessments for prospective Limited Partners

- Fund Documentation: Review of Limited Partnership Agreements, side letters, and DDQs (with legal/compliance input)

- Investment Management

- Deal Execution: Investment decisions

- Portfolio Management: Ongoing monitoring and valuation of investments

- Performance Assessment: Regular evaluation of portfolio companies and exit planning

- Regulatory Compliance

- Regulatory Filings: FCA submissions, AIFMD reporting, and other mandatory disclosures

- Compliance Program: Annual compliance reviews and ongoing regulatory obligations

- Risk Management: Implementation and oversight of risk management framework

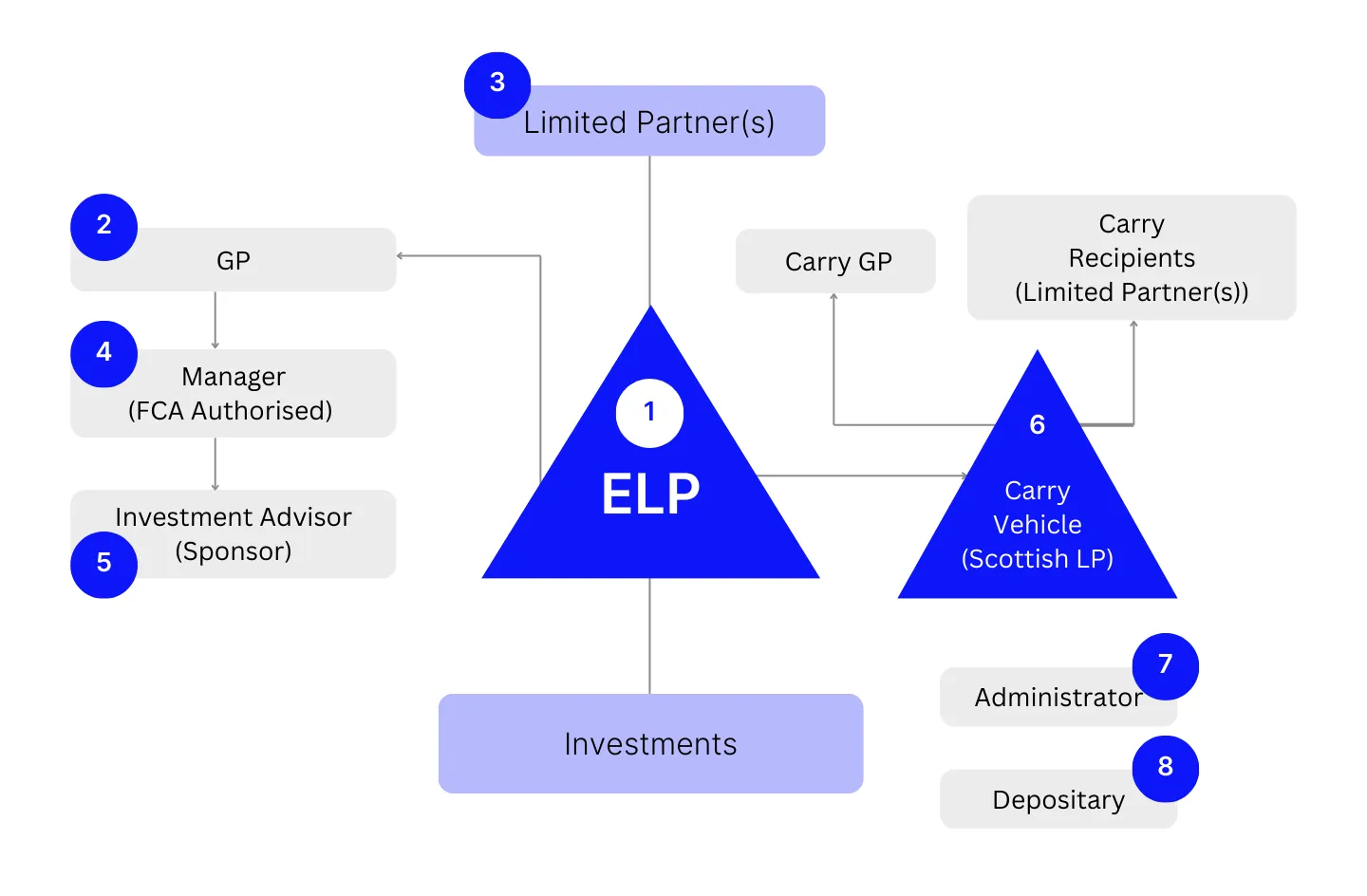

How Does a Host AIFM Structure Work?

A hosted fund structure involves multiple entities, each with distinct responsibilities:

- Private Fund Limited Partnership (PFLP): The Private Fund Limited Partnership is the standard UK fund structure for venture capital/private equity funds, requiring at least one GP and one or more LPs.

- General Partner (GP): The fund’s governing entity, typically controlled by the sponsor. It has unlimited liability and can contractually bind the fund. It will delegate the fund management to the (host) AIFM (the GP cannot carry on these functions itself without having its own FCA authorisation). To manage risk, it’s typically structured as a separate, low-capitalised entity.

- Limited Partners (LPs): Investors who contribute capital to the fund, with their liability restricted solely to the amount of their investment.

- Alternative Investment Fund Manager (AIFM): The FCA-regulated entity responsible for portfolio and risk management. It ensures compliance and retains final decision-making authority, even when delegating investment advice.

- Investment Adviser: In a structure with a host AIFM, the AIFM will sub-delegate deal sourcing and associated tasks to the Sponsor/ Investment Adviser. Due to regulations governing investment advice and deal-making, the sponsor/ investment adviser usually becomes an appointed representative of the host AIFM to enable it to perform those duties.

- Fund Administrator: Manages investor reporting, NAV calculations, and back-office functions. (Note: This service can be provided by bunch.)

- Depositary: Oversees asset safeguarding, cash flow monitoring, and regulatory compliance (if required under AIFMD). Only required for full-scope AIFMs (see section below).

- Carry Vehicle: Typically structured as a Scottish Limited Partnership (SLP), it is used for receiving carried interest and is often also the vehicle through which the sponsor's commitment (i.e. "GP Commit") is made, benefiting from its separate legal personality.

What are the differences between Carry entity, Team entity or Founding Partner (FP) entities?

These terms are largely interchangeable and refer to the entity through which carried interest is paid and/or the team invests. This entity might be called the Carry Partner or Founding Partner, depending on context. For example, in an LPA, the same vehicle may be referred to as the Carry Partner (for carry) and the Founder Partner (for GP commit). While colloquially referred to as the "GP commit," the investment typically doesn't flow through the general partner entity itself, but through this separate vehicle.

By structuring the fund this way, the AIFM maintains full regulatory responsibility, while the investment team focuses on investments and advisory functions within the regulatory framework.

Can Fund Sponsors Retain Management Functions In-House?

One of the most common questions fund sponsors ask is whether they can keep certain management functions in-house while using a host AIFM.

The short answer? Partially.

Fund management is a regulated activity requiring FCA authorisation. If a fund sponsor does not hold its own FCA licence, it cannot act as the manager of the fund (or as a delegated portfolio manager – i.e. it can't make investment decisions). However, it can still play a key role in sourcing deals and monitoring investments.

To enable this, the sponsor is typically appointed as an investment advisor to the AIFM. Since investment advice and deal arrangement are also regulated activities, the sponsor often becomes an Appointed Representative (AR) of the host AIFM. This allows it to operate under the AIFM’s regulatory oversight while engaging in investment advisory activities. Alternatively some AIFMs operate a secondment model, which sees the individuals employed by the sponsor seconded to the AIFM in order to source investments/take investment decisions from within the AIFM itself.

However, the AIFM must retain ultimate responsibility for portfolio and risk management— meaning it must maintain genuine oversight and decision-making power to remain compliant.

Is My Fund a Collective Investment Scheme (CIS)?

Most funds structured as Private Fund Limited Partnerships (PFLPs) fall under the Collective Investment Scheme (CIS) classification under the Financial Services and Markets Act 2000 (FSMA).

Operating a CIS without FCA authorisation is unlawful unless an exemption applies. The host AIFM model addresses this by allowing the fund to operate under the AIFM’s regulatory permissions, ensuring compliance with FSMA requirements.

FCA Authorisation: Full-Scope vs. Sub-Threshold AIFM

Fund managers considering the host AIFM model should understand the regulatory distinctions:

- Full-Scope AIFM: A Full-Scope AIFM is one which has assets under management (AUM) across the various alternative investment funds it manages exceeding €500M (€100M for leveraged or open-ended funds). If you are raising a larger fund (although noting that LP commitments do not count towards AUM until drawn) you may therefore need to engage with a Full-Scope Host AIFM. Previously a Full-Scope AIFM would have the benefit of being able to market its funds on a pan-European basis, but that has not been the case for UK AIFMs since the UK left the EU, so there are no particular regulatory benefits to using a Full-Scope AIFM.

- Sub-Threshold AIFM: A Sub-Threshold AIFM is one which has AUM below the thresholds set out above. This kind of AIFM typically still requires full FCA authorisation (a process that can take over 12 months) but once regulated it is subject to a streamlined regulatory framework for smaller funds. If you are raising a smaller fund you may be able to work with a Sub-Threshold AIFM to streamline the regulatory requirements applying to your fund.

Brexit & Fund Marketing Considerations

Since Brexit, UK fund managers have lost access to the EU marketing passport, meaning fundraising within the EU is now subject to individual country regulations under National Private Placement Regimes (NPPRs). You may also be required to register for "pre-marketing" as well (e.g. before sending marketing presentations about the fund).

If your LPs have asked you for information about the fund rather than you providing it at your own initiative, that may constitute a reverse solicitation for which no NPPR registration is required.

Final Thoughts

The host AIFM model provides a compliant and efficient pathway for fund managers looking to launch quickly while navigating complex UK regulatory landscapes. By working with an experienced AIFM, sponsors can streamline operational complexity and focus on their core investment strategy.

However, choosing the right host AIFM is critical. Fund sponsors should assess potential AIFM partners based on their regulatory track record, operational capabilities, and alignment with the fund’s long-term strategy.

For a deeper dive into structuring and authorisation, see ‘Working with a Host AIFM: What You Need to Know’.

The best already build on bunch

.webp)